Can I pay to clear my credit history? What is the best credit repair service? How much does credit repair cost?

These and many others are some of the questions people ask when in need of repairing their credit. If you’ve had an overdue student loan or high credit balances, then your credit score is below average.

With poor credit, it’s difficult to qualify for financial products like mortgages, car loans and credit cards. Even if you do, the interest rates will be so high meaning you’ll get to pay more. For example, if you have a credit score of 600 or below, you will get a high rate on a home mortgage compared to a person with a credit score of 750+.

The good news is, you can improve your credit score. Research shows that 48% of people who used credit repair services for 6+ months saw an increase of 100+ points to their credit score.

Want to know how to improve your bad credit?

In this post, we’ll discuss how to repair your bad credit.

Sample Letters and Forms

The average FICO score in the US is 700 or higher. In fact, an Experian survey revealed that 59% of Americans now have a FICO score of 700 or higher. In 2019, the average credit score was 703 compared to 701 in 2018.

This signifies that many people are becoming more educated on their credit. What experts noted is that late payment rates for several credit products decreased over the past decade. Credit balances experienced moderate growth, providing confidence to lenders.

What Does a Credit Score of 700 or Higher Mean?

A credit score of 700 or higher is good. If you have such a credit score, you should feel confident applying for any financial product. For example credit cards, mortgage and car loans, among others.

Let’s assume you have a credit score of 700 and higher. If you seek a car loan, the lender may offer you 3.39% for 60 months.

As you can see, you get to save a lot of money on your auto loan. Similar savings extend to people who want to refinance their mortgages and student loans.

Here is a table showing the FICO score and rating.

Credit Rating

Very Poor: 300 to 597

Fair: 580-669

Good: 670-739

Very Good: 740-799

Exceptional: 800-850

If you want to repair your credit score, there are a couple of documents you need to be aware of. The good news is, there are templates available online for each of these documents.

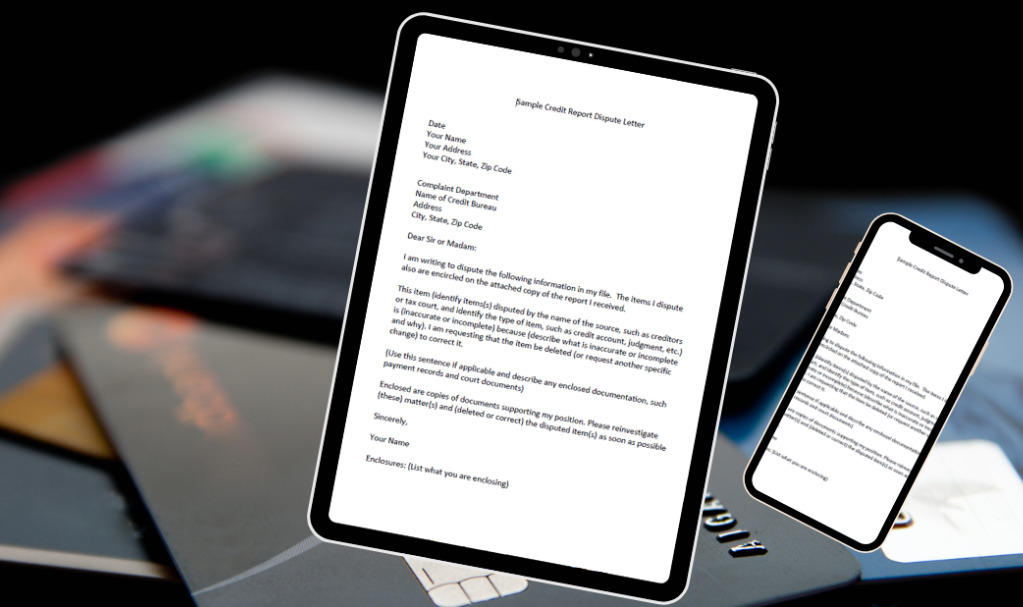

Credit Dispute Letter

If you suspect a financial institution is reporting incorrect details to credit bureaus, send a credit dispute letter. This letter will require the organization to investigate and resolve the issue in 30 days.

Details in your credit report that are subject to dispute include:

=> Late payments

=> Credit inquiries

=> Collection accounts

It’s essential before sending out a credit dispute letter to ensure that your case is compelling. Always send the letter to the credit bureau with all relevant documents.

Here is a Sample Letter for Disputing Errors on your Credit Score.

Method of Verification Letter

There are credit bureaus that may be reluctant to correct or remove disputed errors in your credit report. By sending a method of verification letter, you’re requesting the credit bureau to provide proof that supports their decision.

In your letter, you must demonstrate that the credit bureau failed to conduct due diligence or mismanaged the process. This is useful in case you decide to take your case to court.

Here is a Method of Verification Sample Letter.

Credit Inquiry Removal Letter

Have you discovered any hard or soft inquiries on your credit report? Would you like to remove them? To do so, you must write a credit inquiry removal letter and send it to each credit bureau that lists an inquiry.

What you need to know is that inquiries affect your credit score up to 1 year and they’re listed up to 2 years in your credit report. The more inquiries you have, the more your credit score gets affected.

Use this Sample Credit Inquiry Removal Letter to remove inquiries from your credit report.

How to Get and Read Your Credit Report

If it’s your first time, credit reports can be confusing. What you need to know is that a credit report is a snapshot of your financial information. Also, the law requires that you review the report every 12 months.

How Do I Get My Credit Report?

There are three significant US credit bureaus, namely:

=> Experian

=> Equifax

=> TransUnion

In 2003, federal law required these three organizations to set up a central online resource for credit report requests. That platform is AnnualCreditReport.com. To request your credit report, you can download the request form and mail it to:

Annual Credit Report Request Service

Box 105281

Atlanta, GA 30348-5281

Another option is to visit AnnuaCreditReport.com. Click “Request Yours Now”, and the site will redirect to a webpage detailing the steps. Fill out a form to request one, two, or three credit reports.

You’ll have to answer a few questions, so have your records with you. The form will require you to provide your personal identification information that includes:

Name

Address

Social Security Number

Date of birth

After providing your basic information, the site will allow you to select your credit report from any of the three credit bureaus. Just check the boxes beside the credit bureaus logos.

Once you have your credit report, print to look at it later. You can get your free credit report every 12 months. But if you need to review it frequently, call the Annual Credit Report Request Service.

Here is a sample credit report.

How to Read Your Credit Report

Start by reading the “Personal Information” section. By reading this section, you ensure that the credit report is yours and not for another person who shares your name. Make sure you double-check the details.

Next, move to your credit history. This section includes total loan amounts, open and paid credit accounts. It also consists of any accounts you share with someone else, late payments, and loan balances.

Read and reread this section. Check for accounts opened without your consent. If you closed a credit card account, make sure it’s closed in your credit report.

The next section is public records. In this section, financial activity such as tax liens, bankruptcy and judgments are usually listed. What you need to know is that some of these details can stay on your credit report for up to 10 years.

If you find mistakes in this section, have them cleared.

After the public records section, you have inquiries. Here, your hard and soft inquiries are usually listed. Hard inquiries can cause your credit score to drop by several points. So it’s crucial to make sure you have given your permission for them to be in your credit report.

How to Stop Collection Agencies

Is the debt collector calling you multiple times a day? Has the debt collector contacted your family or employer? Do you feel like changing your phone number to stop these calls?

If calls from debt collectors are annoying you that you feel like changing your phone number, then you have come to the right place.

The first thing you need to know is that all debt collectors must abide by the Fair Debt Collection Practices Act. As such, they’re not allowed to call you regarding a debt you don’t owe.

When a debt collector makes contact with you for the first time, he or she must verify the debt is yours. If the debt collector cannot verify if the debt is yours, they are not allowed to contact you anymore.

Debt collectors are also not supposed to call you before 8 AM or after 9 PM.

There are several ways of stopping debt collection agencies. You can hang up on a debt collector if he or she calls you repeatedly. This is because they violate the Fair Debt Collection Practices Act.

Besides hanging up on the debt collector, you can send them an email or letter asking them to communicate with you via writing. By requesting the collector to send letters, it gives you a chance to have records which can act as evidence in a lawsuit.

Speaking of letters, you can write a cease and desist letter to the debt collector. This letter should state that the debt collector cease and desist from communicating with you. What you need to know is that this only works with third-party collectors.

How to Avoid Credit Scams

Study after study has shown that millions of Americans fall victim to credit fraud. This costs the national economy billions of dollars. If you are a victim of credit fraud, you need to know that it’s a problem. Lucky for you, there are ways of avoiding credit scams.

Add a Fraud Alert

Add a fraud alert to your credit report. To do so, visit the Experian fraud center or any of the other two credit bureaus. By adding a fraud alert, you will receive notifications. They will alert you of any financial activity before extending credit in your name.

Use Secure Passwords

Many people choose to use simple passwords like “1234” or even the word “password.” What you need to know is that hackers and scammers can break such passwords using simple hacking scripts or tools.

To prevent this, use secure passwords that include alphanumerics. You can strengthen the password by adding characters.

Monitor Your Account Closely

How frequently do you check your credit card activity? If a week or month goes by without checking your account activity, you may be a victim of credit fraud. By closely monitoring your account activity, you will be sure that your information is not compromised.

Besides monitoring your account, check your bank statements too. If you discover signs of fraud, notify your bank.

Don’t Respond to Fraudulent Emails or Texts

The most common forms of credit fraud involve misleading ads, texts, fake trial offers, and online shopping scams. If you receive texts or emails that seem suspicious or too good to be true, delete them. Do not respond or provide your personal details to the scammer.

Also, do not click any links in the email even if they look legitimate. This is how phishing scams lure you into providing your login information on their fake website. To log into your account, visit the official site directly.

How to Get Your Finances Back on Track

Are you drowning in debt? If you find yourself in the never-ending cycle of overdrafts, credit card repayments, and others, don’t get discouraged. There are ways to get back on track.

Accept You Are in Trouble

Research shows that consumer debt in the US hit $4.2 trillion as of 2019. Collectively, Americans own 10% of their disposable income to non-mortgage debts like credit cards and car loans.

To get back on the financial track, accept you are in trouble. Denying will not get you out of the position you are in.

Track Your Expenditure

Do you know how much you spend on coffee or pizza every month? If you don’t, starting from today, track every penny you spend. By the end of the month, you will know how much you spend on food, utility bills, shopping, and eating out, among others.

Have Realistic Financial Goals

Many people find themselves struggling with money or back in debt just because they failed to make realistic financial goals. To get your finances back on track, make a twelve-month plan. It should include a plan of wiping out your credit card debt and other loans.

Also, include how to save for a holiday, for retirement, and investing.

Get a Part-Time Job

Today, there are thousands of online opportunities which can boost your income. Such opportunities include copywriting, logo design, web design, proofreading, and many more. By spending two to three hours every day, you can make $300 to $1000 every week or month.

Not only will this supplement your income, but, it will help you get your finances back on track.

Final Thoughts

There you have it. The complete guide to improving your credit score and taking control of your finances. We hope that this post will guide you in making sound financial goals and get you in the habit of reviewing your credit report every three months.

If you discover an error, take the appropriate steps to have it removed. Alternatively, you can hire a reputable credit repair company. This will save you time and money.

{kind=link}